Show figure code

df <- bayestestR::simulate_correlation(n=500, r=0.7)

df |>

ggplot(aes(x=V1, y=V2)) +

geom_point() +

geom_smooth(method="lm", formula = 'y ~ x', se=FALSE, linewidth=2, color="red") +

theme_bw()@ LaPsyDé

![]()

df <- bayestestR::simulate_correlation(n=500, r=0.7)

df |>

ggplot(aes(x=V1, y=V2)) +

geom_point() +

geom_smooth(method="lm", formula = 'y ~ x', se=FALSE, linewidth=2, color="red") +

theme_bw()df |>

ggplot(aes(x=V1, y=V2)) +

geom_point() +

geom_smooth(method="lm", formula = 'y ~ x', se=FALSE, linewidth=2, color="red") +

stat_ellipse(type = "norm", color="blue", linewidth=2) +

theme_bw()ggplot(df, aes(x=V1, y=V2)) +

geom_point(alpha=0) +

geom_vline(xintercept = 0, linetype="dotted") +

geom_abline(intercept = 1, slope = 3, color="red", linewidth=2) +

geom_segment(aes(x = 0, y = 1, xend = 1, yend = 1), linewidth=1,

color="green", linetype="dashed") +

geom_segment(aes(x = 1, y = 1, xend = 1, yend = 4), linewidth=1,

color="green", linetype="solid", arrow=arrow(length = unit(0.1, "inches"))) +

geom_segment(aes(x = 0, y = 0, xend = 0, yend = 1), linewidth=1,

color="blue", linetype="solid", arrow=arrow(length = unit(0.1, "inches"))) +

geom_point(aes(x = 0, y = 0), color="purple", size=8, shape="+") +

labs(x="x", y="y") +

theme_bw() +

coord_cartesian(xlim = c(-1, 1.5), ylim = c(-3, 4))p <- mtcars |>

ggplot(aes(x=qsec, y=mpg)) +

geom_point(alpha=0.7, size=6) +

geom_smooth(method="lm", formula = 'y ~ x', se=FALSE, linewidth=2) +

geom_segment(aes(x = qsec, y = mpg, xend = qsec, yend = predict(lm(mpg ~ qsec, data=mtcars))),

color="red", linetype="dotted", linewidth=1) +

theme_bw() +

labs(x="x", y="y", title="The residuals are the vertical distances between each point and the line.")

p2 <- data.frame(Error=insight::get_residuals(lm(mpg ~ qsec, data=mtcars))) |>

ggplot(aes(x=Error)) +

geom_histogram(bins=10, fill="grey", color="black") +

geom_vline(xintercept = 0, linetype="dashed") +

geom_density(data=data.frame(Error=bayestestR::distribution_normal(n=100, sd = 2)),

aes(y=after_stat(density)*40), color="#F44336", linewidth=1, adjust=1) +

geom_density(data=data.frame(Error=bayestestR::distribution_normal(n=100, sd = 3)),

aes(y=after_stat(density)*50), color="#FF5722", linewidth=1, adjust=1) +

geom_density(data=data.frame(Error=bayestestR::distribution_normal(n=100, sd = 4)),

aes(y=after_stat(density)*60), color="#FF9800", linewidth=1, adjust=1) +

geom_point(aes(y=0), size=10, shape=16, alpha=0.3) +

theme_bw() +

coord_flip() +

labs(y = "Density")

p + theme(plot.title = element_blank()) | p2model <- lm(mpg ~ qsec, data=mtcars)

p <- mtcars |>

ggplot(aes(x=qsec, y=mpg)) +

geom_smooth(method="lm", formula = 'y ~ x', se=FALSE, linewidth=2) +

theme_bw()

# Function to add normal distribution curves

add_normals <- function(p, model) {

sigma <- summary(model)$sigma # Standard deviation of residuals

n <- 100 # Number of points for each curve

for(i in 1:nrow(mtcars)) {

x_val <- mtcars$qsec[i]

y_pred <- predict(model, newdata = data.frame(qsec = x_val))

# Create a sequence of y values for the normal curve

y_seq <- seq(y_pred - 3*sigma, y_pred + 3*sigma, length.out = n)

density <- dnorm(y_seq, mean = y_pred, sd = sigma)

# Adjust density to match the scale of the plot

max_width <- 1 # Max width of areas

density_scaled <- (density / max(density)) * max_width

# Create a dataframe for each path

path_df <- data.frame(x = x_val + density_scaled, y = y_seq)

path_dfv <- data.frame(x=path_df$x[1], ymin=min(path_df$y), ymax=max(path_df$y))

# Add the path to the plot

p <- p +

geom_segment(data = path_dfv, aes(x = x, xend=x, y = ymin, yend=ymax),

color = "#FF9800", linewidth = 0.7, alpha=0.8, linetype="dotted") +

geom_path(data = path_df, aes(x = x, y = y),

color = "#FF9800", linewidth = 1, alpha=0.8)

}

p

}

# Create the final plot

p <- add_normals(p, model) +

geom_segment(aes(x = qsec, y = mpg, xend = qsec, yend = predict(lm(mpg ~ qsec, data=mtcars))),

color="red", linetype="solid", linewidth=1) +

geom_point(alpha=0.8, size=6)

p# Plot t-distribution

x <- seq(-5, 5, length.out = 1000)

y <- dt(x, df=30)

df <- data.frame(x = x, y = y)

t_value <- 2.790

df$Probability <- ifelse(df$x < -t_value, "< -t", "Smaller")

df$Probability <- ifelse(df$x > t_value, "> +t", df$Probability)

df |>

ggplot(aes(x = x, y = y)) +

geom_line() +

geom_area(aes(x = x, y = y, fill = Probability), alpha = 0.5) +

geom_segment(data=data.frame(x=t_value, y=0),

aes(xend = t_value, yend = dt(t_value, df=30)),

color="red", linetype="solid", linewidth=1) +

geom_point(data=data.frame(x=t_value, y=dt(t_value, df=30)), color="red", size=3) +

theme_minimal() +

scale_fill_manual(values = c("red", "red", "grey")) +

labs(x = "\nt-values - standardized coefficient under the null hypothesis", y = "Probability",

title = paste0("t-Distribution (df=30); ", "t-value = ", round(t_value, 2), "\n"))model <- lm(mpg ~ qsec, data=mtcars) # Fit linear regression

true_coef <- coef(model)[2] # Extract slope coefficient

coefs <- c() # Initialize an empty vector of coefs

for (i in 1:5000) { # Repeat the process 500 times

new_sample <- mtcars[sample(1:nrow(mtcars), replace = TRUE), ] # Sample new data

new_model <- lm(mpg ~ qsec, data=new_sample) # recompute the model

coefs <- c(coefs, coef(new_model)[2]) # Append the coef to the vector

}data.frame(coefs = coefs) |>

ggplot(aes(x = coefs)) +

geom_density(fill="orange") +

geom_vline(xintercept = true_coef, color="red", linetype="dashed", linewidth=2) +

theme_minimal() +

labs(x = "Coefficient", y = "Frequency",

title = "Distribution of coefficients from 5000 bootstrapped samples\n") +

coord_cartesian(xlim = c(-0.5, NA))

bayestestR exists to convert between the two indices.

bayestestR::p_to_pd(c(0.05, 0.01, 0.001), direction = "two-sided")[1] 0.9750 0.9950 0.9995bayestestR::pd_to_p(c(0.90, 0.95), direction = "two-sided")[1] 0.2 0.1

data.frame(Coefficient = coefs) |>

ggplot(aes(x=Coefficient)) +

geom_density(fill="blue") +

geom_area(data=data.frame(x=c(-0.42, 0.42)), aes(x=x, y=2), fill="red", alpha=0.5) +

coord_cartesian(xlim=c(-0.6, 3.5))

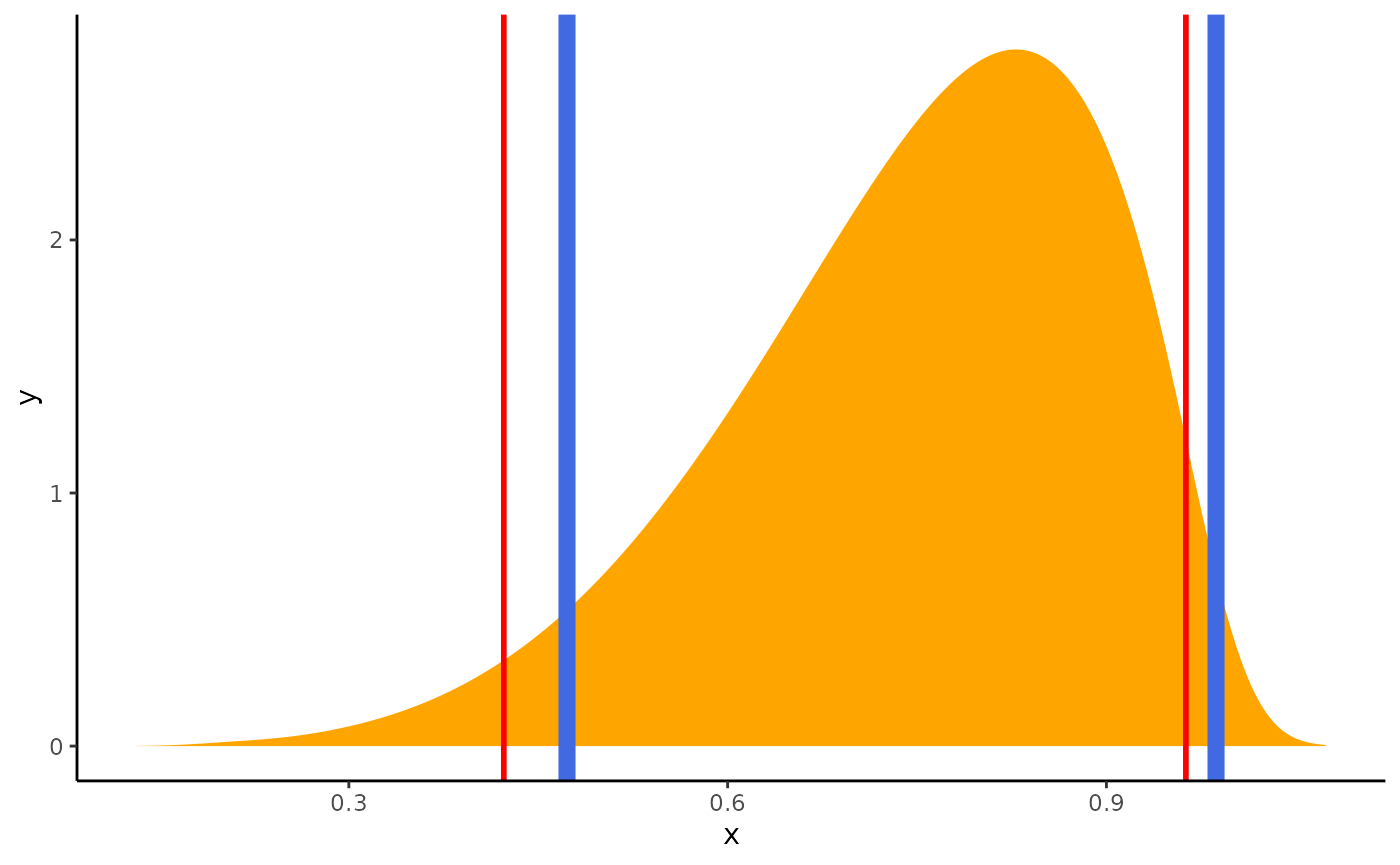

bayestestR::rope(coefs, range = c(-0.42, 0.42), ci = 1.00)# Proportion of samples inside the ROPE [-0.42, 0.42]:

inside ROPE

-----------

0.66 % # ci=0.95 is the default setting for rope()

result <- bayestestR::rope(coefs, range = c(-0.42, 0.42), ci = 0.95)

result# Proportion of samples inside the ROPE [-0.42, 0.42]:

inside ROPE

-----------

0.00 % # The results can be plotted

plot(result)

Thank you!

![]()